Posts Tagged ‘govcon’

Why You Need a Government Contracts CPA to Work on Your Government Contracting Business Taxes

Taxes are an essential element of financial planning for any business, but when it comes to government contracting, the stakes are significantly higher. The interplay of federal regulations, cost accounting standards, and tax codes requires specialized expertise to ensure compliance and optimize financial performance. A Government Contracts CPA (Certified Public Accountant) helps contractors meet these…

Read MoreThe Cornerstone of Winning Bids: Understanding Proposal Adequacy for Government Contractors

In the competitive realm of government contracting, the difference between securing a contract or facing rejection often hinges on a straightforward but critical factor: proposal adequacy. Even contractors adept at demonstrating their capabilities and strengths find ensuring a proposal meets every nuance and stipulation of a Request for Proposal (RFP) to be a complex challenge.…

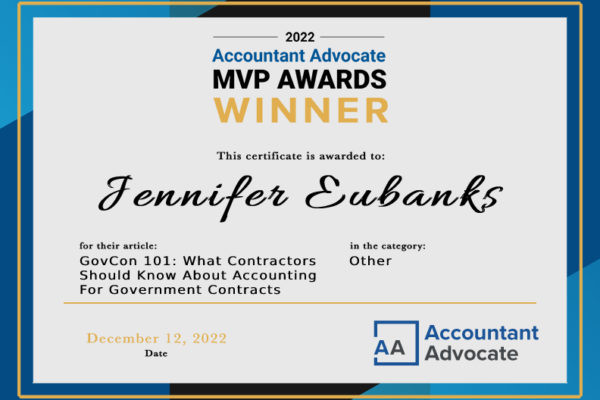

Read MoreJennifer Eubank’s Article Wins 2022 Accountant Advocate MVP Awards.

Jennifer Eubank’s article GovCon 101: What Contractors Should Know About Accounting For Government Contracts,” has won 1st place in the 2022 Accountant Advocate MVP Awards Other category! To learn more, visit here.

Read MoreGovCon 101: What Contractors Need To Know About Indirect Rates

Jennifer Eubanks recently authored the council post, GovCon 101: What Contractors Need To Know About Indirect Rates In the first article of this series of articles related to selling to the federal government, I discussed federal acquisition regulations (FAR), cost accounting standards (CAS) and the types of contracts issued by government agencies. In the second article, I expanded…

Read MoreGovCon 101: What Contractors Should Know About Accounting For Government Contracts

Jennifer Eubanks recently authored the council post, GovCon 101: What Contractors Should Know About Accounting For Government Contracts In a prior article, I wrote about the appeal of counting the Federal Government as a customer, because of the size of the government’s budget, as well as its creditworthiness. In that article, I discussed Federal Acquisition Regulations…

Read MoreGraduate Certificate in Accounting for Government Contracts Soon Available at George Mason University

At CPA Department, we bring to the table over 30 years of experience in Government Contract Consulting. We have long partnered with government contracts in order to not only assist with financial decisions, audits, and taxes, but also to help fulfill the unique needs in the field. Since it is vital for government contractors to…

Read MoreCPA Department’s Jennifer Eubanks attending Capitol Hill Week to Promote PPP Legislation on June 11

We’re excited to have a direct line of communication with the Members of Congress that represent us. Now more than ever, our small business voices need to be heard!

Read MoreTax Implications of Coronavirus Relief

A number of tax implications evolve as a result of relief provided by the Coronavirus Aid, Relief and Economic Security (CARES) Act, and the Families First Coronavirus Response Act (FFCRA). We’ve created a summary of information as it has evolved to date.

Read MoreMurky Waters for Government Contractors Receiving PPP Funds

Government contractors, constantly vigilant and monitoring compliance with Federal Acquisition Regulations are faced with unprecedented uncertainty and questions surrounding acceptance of Paycheck Protection Program (PPP) funds and payments under Section 3610 of the CARES Act. Contractors must consider a) the ban against ‘double dipping’ of funds and b) must also consider that loan forgiveness under the PPP may be interpreted as a credit due back to the government in accordance with FAR 31.201-1 (a).

Read More